This article first appeared in Grant’s Interest Rate Observer, Vol. 40, No. 18 published on 30 September 2022. It is republished here with permission from Grant’s Financial Publishing, Inc.

“We went very aggressively net short in the middle of August,” Henry Maxey, chief investment officer of Ruffer, LLP, London, was telling Grant’s over the transatlantic blower on Monday. “That position we’ve largely held. We are the least exposed, and we are net short for the first time in our history.”

In London, currencies were crashing, yields surging and equities wobbling. Things were in such a state that a sympathetic tube rider offered an ashenfaced Ruffer small-cap fund manager a seat. What the average net-long English investor must look like today is anybody’s guess.

Maxey, whose prophetic ideas on the volatility of the inflation problem have featured in these pages before (eg Grant’s, July 8), did not decide to go net short on a hunch. For months, he’s been working up a theory about the intersection of interest rates, asset prices and liquidity.

Our reading of the situation, informed by Maxey, goes like this: The upside lurch in short-term rates puts pressure on stock and bond prices. Post-2007-2009 financial regulation crimps liquidity in unpredictable ways. What began as an interest rate shock will thus become a liquidation event.

Fundamental to Maxey’s thinking is the migration of systemic risk to asset managers from banks following the global financial crisis. “It can’t be so that the only purpose of banking is to stop banks [from] going bankrupt,” a Nordic banker futilely protested as governments moved heaven and earth to prevent an exact recurrence of the 2007-2009 crisis.

Of course, financial risk didn’t disappear; it moved, and it moved to the investment managers whose clients, under the spell of QE and ultralow interest rates, were shifting heavily into stocks and credit. Note, Maxey observes, that the balance sheet of an asset manager is inflexible. It expands with investment inflows, contracts with investment outflows. Banks, assuming that they have sufficient capital and regulatory leeway, can absorb risk even as others shun it: “They can flex their balance sheets,” says Maxey, “and, as a result, they either directly or indirectly set the tempo of markets.”

A second precept of the Maxey approach is that fast-rising money-market yields will strip funds from low-yielding bank accounts. Losing deposits, banks will curtail lending.

Financial historians and senior citizens well recall the American disintermediation drama of the 1970s. Inflation lifted market interest rates, though not deposit rates, which the Fed’s Regulation Q had capped. It was a dull saver who failed to notice that higher returns were available outside the walls of his or her bank. Newfangled money-market mutual funds welcomed the aggrieved former depositors.

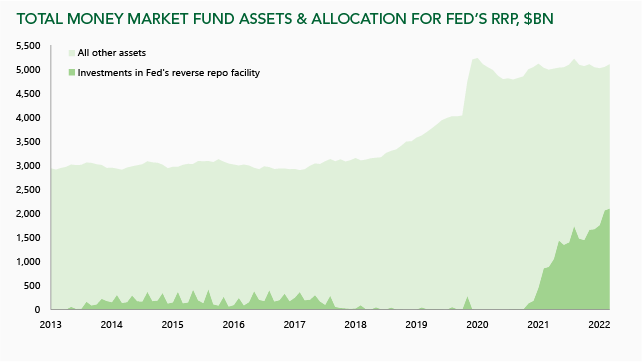

A similar dynamic is at work today, but with sums in the trillions rather than the mere billions. In the regulatory drive to forestall another 2007-2009, most money-market mutual funds chose to become “government-only” funds. In exchange for the privilege of posting an unvarying net asset value (always a popular feature with the investor base), they agreed to forego such once common money-fund assets as commercial paper and banker’s acceptances. Their new opportunity set consisted of short-dated Treasury bills.

However, there is now another option available to the government-only manager. He or she can choose between, on the one hand, a 30 day Treasury bill yielding 2.6%, or, on the other, a 24 hour investment in the Fed’s overnight reverse repo facility, which delivers 3.05%. Needless to say, the RRP facility – which, pure and simple, exchanges the Fed’s securities for cash is growing like a dandelion. What’s shrinking, in consequence, is the flexibility – the “risk-taking potential,” as Maxey puts it – of the banking system.

There are counterarguments. One could conjecture that there’s plenty of banking liquidity to go around – wasn’t it the very redundancy of dollars that caused the inflation that upended the bond market?

Or one could object that the safety and soundness panic of 2010-2011 long ago robbed the banking system of its resiliency. Alluding to such innovations as the “liquidity coverage ratio,” the “supplementary leverage ratio” and the “Volcker rule,” Jamie Dimon, CEO of JP Morgan Chase & Co, pressed then Fed Chairman Ben S. Bernanke, Ph.D, in June 2011: “Has anyone looked at the cumulative effect of all these regulations, and could they be the reason it’s taking so long for credit and jobs to come back?” No, Bernanke allowed, no one had-perhaps no one could.

Anyway, Maxey argues that the unemployed dollars called bank reserves are not so excessive as many suppose and that continued growth in the RRP facility will contribute to the shrinkage of these balances. Such losses, in turn, will check the banks’ capacity to lend and borrow.

In the innocent, long-ago world of 2007, the banking system somehow managed to get by on less than $10 billion of excess reserves. Under the “ample reserves” regime of the Powell Fed, which followed years of QE, it holds $3.3 trillion’s worth of this monetary padding. Along with other great known unknowns of the world today-the course of the Russian-Ukrainian war, the intentions of the Bank of Japan regarding the 10 year JGBs whose 25 basis point yield it continues to hold hostage, the track of the renminbi-dollar exchange rate, etc the minimum prudent level of American bank reserves is a mystery.

In mid-September 2019, $1.3 trillion had seemed a more than sufficient cushion, yet it proved explosively insufficient when the repo rate on government securities lurched to almost 10%, badly rattling the Fed and inducing the resumption of modified QE operations in the shape of $60 billion’s worth of monthly T-bill purchases. The purpose of this intervention, according to the mandarins, was to restore “smooth market functioning.” That functioning is noticeably less smooth today, yet, for the inflation-preoccupied Fed, a restart of QE would appear decidedly off-message.

Is there a level of reserve balances that would flip the liquidity switch to ‘contraction’ from ‘expansion’? Maxey says he knows of none and that, anyway, the point is not the level but the movement. Recall, he says, the story of the fellow who tumbles out of a 50 story window. “So far, so good,” the chap repeats to himself as he plunges to the street.

Thus, it’s the shifting of funds from one department of the liability side of the Fed’s balance sheet, ie, ‘reserves,’ to another, ie, ‘RRP’ that counts: not so much the level of those liabilities but their composition, and their motion.

Why should it matter? Because, Maxey replies, reserve balances support banking activity-credit creation, whether for business activity or financial operations. There is no such multiplier in the federal parking lot of the RRP: The high-yielding dollars are inert.

With all that said, Maxey reckons that between $2.2 trillion and $2.6 trillion might prove a decent minimum level of bank reserves today. Thus, a migration of between $600 billion and $1 trillion or so of reserves into the RRP facility could spell trouble. But, again, you don’t have to wait for the terminal point to know you’re in trouble. “Everyone looks at the system and says there is not going to be any problem for the next $600 billion to $1 trillion of reserves outflow. I’m saying that there is a problem as that outflow occurs. It’s a problem for wider asset markets.” And a problem, Maxey adds, of the moment: “The next couple of months are going to be the most extreme.”

On Tuesday, the RRP facility housed $2,327 billion in deposits; a year ago, it held just $1,297 billion.

We observed that all this is happening in the context of one major central bank still pinning its policy rate below zero and still doing QE. What would happen to the global liquidity situation if the Bank of Japan turned on its heel and lifted its policy rate above zero?

Nothing very good, Maxey allowed, particularly if Japanese corporations decided to repatriate a portion of their substantial foreign assets.

We asked our English friend if compelling investment values had begun to surface in his own backyard. ’Tm preferring to wait,” Maxey replied. “Investors are treating the UK like an emerging market, and I think the time will come when the dollar and dollar assets are sold. Then you want to look at emerging markets, and the UK has become the most developed of the emerging markets. I expect UK assets will be an interesting place to be and that it will be a very good stock picking environment. The characteristics of the stocks you want are things that are going to benefit from international nominal growth being relatively resilient and a UK sterling cost base. Professional-services businesses, engineering businesses. They are quite small opportunities, but there are quite a few of them in the UK.”

But make no mistake, Maxey says: A liquidation will likely precede the opportunity. What kind of liquidation? A waterfall of the things that can be sold, as distinct from the ones that can’t. Private equity, private real estate and private credit owe their booming popularity to the very fact that they have no tickers, no daily marks.

Beware, then, Maxey closes, of the most popular flavors of the former bull market, among them sovereign debt and big-cap common stocks. Their liquidity is a bullseye.